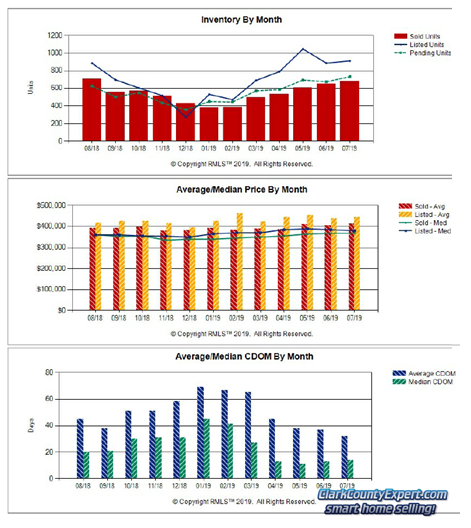

Equity build-up could be one of the biggest advantages to buying a home. There are two distinct dynamics that take place to make this happen: each house payment applies an amount to reduce the mortgage owed and appreciation causes the value of the home to go up.

It is easy to make a projection based on the type of mortgage you get and your estimation of appreciation over the time you expect to own the home. Even conservative estimates can produce impressive results.

Let's look at an example of a home with a $270,000 mortgage at 4.5% for 30 years and a total payment of $2,047.55 payment including principal, interest, taxes and insurance. The average monthly principal reduction for the first year is $362.98. If you assume a 3% appreciation on the $300,000 home, the average monthly appreciation is $750 a month.

The total payment of $2,047.55 less $1,112.98 for principal reduction and appreciation makes the net monthly cost of housing, excluding tax benefits, $934.57. If this hypothetical person was paying $2,500 in rent, it would cost them $1,565.43 more to rent than to own. In the first year, it would cost them over $18,000 more to rent.

Together, the items in this example contribute over $1,100 to the equity in the home . This is one of the reasons a home is considered forced savings. By making your house payments and enjoying increases in value, the equity grows and the net cost of housing decreases by the same amount.

In this same example, the $30,000 down payment grows to $133,991 in equity in seven years. While this is equity build-up, the extraordinary growth is attributed to leverage. Leverage is an investment principle involving the use of borrowed funds to control an asset.

To see what your net cost of housing and the effect of leverage will have on a home in your price range, see the Rent vs. Own. If you have questions or need assistance, ontact Equity build-up could be one of the biggest advantages to buying a home. There are two distinct dynamics that take place to make this happen: each house payment applies an amount to reduce the mortgage owed and appreciation causes the value of the home to go up.

It is easy to make a projection based on the type of mortgage you get and your estimation of appreciation over the time you expect to own the home. Even conservative estimates can produce impressive results.

Let's look at an example of a home with a $270,000 mortgage at 4.5% for 30 years and a total payment of $2,047.55 payment including principal, interest, taxes and insurance. The average monthly principal reduction for the first year is $362.98. If you assume a 3% appreciation on the $300,000 home, the average monthly appreciation is $750 a month.

The total payment of $2,047.55 less $1,112.98 for principal reduction and appreciation makes the net monthly cost of housing, excluding tax benefits, $934.57. If this hypothetical person was paying $2,500 in rent, it would cost them $1,565.43 more to rent than to own. In the first year, it would cost them over $18,000 more to rent.

Together, the items in this example contribute over $1,100 to the equity in the home . This is one of the reasons a home is considered forced savings. By making your house payments and enjoying increases in value, the equity grows and the net cost of housing decreases by the same amount.

In this same example, the $30,000 down payment grows to $133,991 in equity in seven years. While this is equity build-up, the extraordinary growth is attributed to leverage. Leverage is an investment principle involving the use of borrowed funds to control an asset.

To see what your net cost of housing and the effect of leverage will have on a home in your price range, see the Rent vs. Own. If you have questions or need assistance, please feel free to contact me.